Polymarket Liquidity Mining Guide 2026: How to Earn USDC Without Winning a Single Bet

The biggest mistake beginners make on Polymarket in 2026 is thinking you have to win a bet to make money. Specifically, the platform pays daily USDC rewards to traders who provide liquidity by placing limit orders in active markets, regardless of whether those orders ever fill and regardless of whether the underlying outcome resolves in your favor. Furthermore, professional liquidity providers in 2026 are earning between 15% and 80% APY on deployed capital across high-volume markets including US Elections, Fed rate decisions, and major sports outcomes, while their orders sit passively in the order book earning rewards every single minute. This guide covers how the reward formula works, how to set up your first tight-quoting position, what the genuine risks are, and the advanced techniques that professional market makers use to protect their capital while maximising yield.

Market Making vs Gambling: The Fundamental Distinction

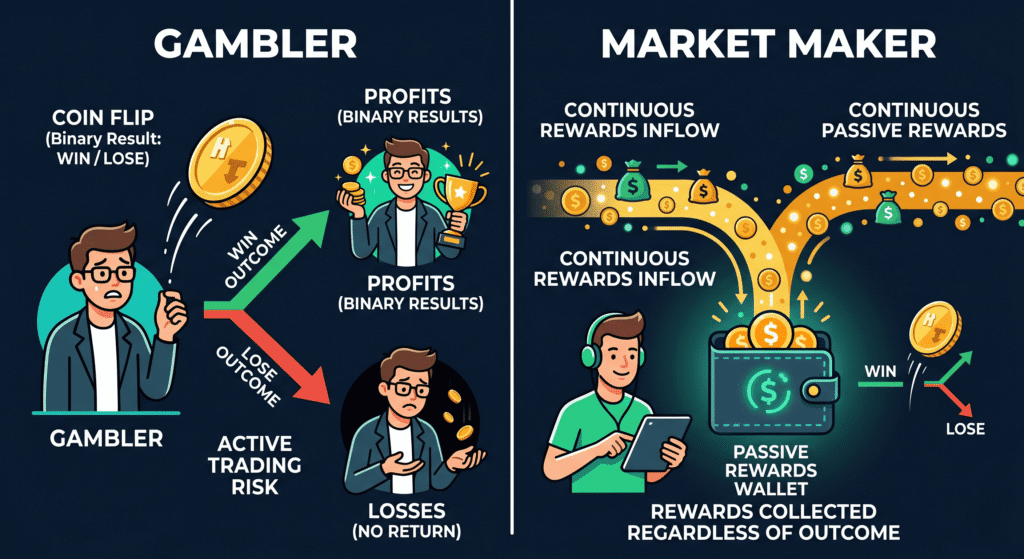

Most Polymarket users are gamblers in the technical sense. Specifically, they take a directional position on an outcome, they win if the outcome resolves in their favor, and they lose if it does not. The expected value of a directional position depends entirely on whether the trader’s probability assessment is more accurate than the market’s implied probability.

Market making is a fundamentally different activity. A market maker does not need to be right about the outcome. Instead, the market maker provides the inventory that directional traders buy and sell, collecting the spread between the bid and ask price on each transaction while also collecting explicit USDC reward payments from Polymarket for maintaining tight liquidity.

Specifically, when a directional trader buys YES shares at 51 cents and the market maker sold those shares at 51 cents while simultaneously holding a NO limit order at 49 cents, the market maker’s profit comes from the 2-cent spread rather than from the outcome itself. Furthermore, Polymarket’s liquidity reward program pays an additional daily USDC incentive on top of the spread income, calculated based on how close to the midpoint the market maker’s orders sit and how large those orders are.

The key practical difference is the sleep factor. Once limit orders are placed, they earn rewards continuously without any further action required. Specifically, rewards accrue every minute the orders sit within the qualifying spread range, whether or not any trades execute against them. A directional trader who goes to sleep while holding a position is exposed to outcome risk overnight. A market maker who goes to sleep while holding limit orders continues earning rewards.

How the 2026 Polymarket Reward Formula Works

The Quadratic Spread Function

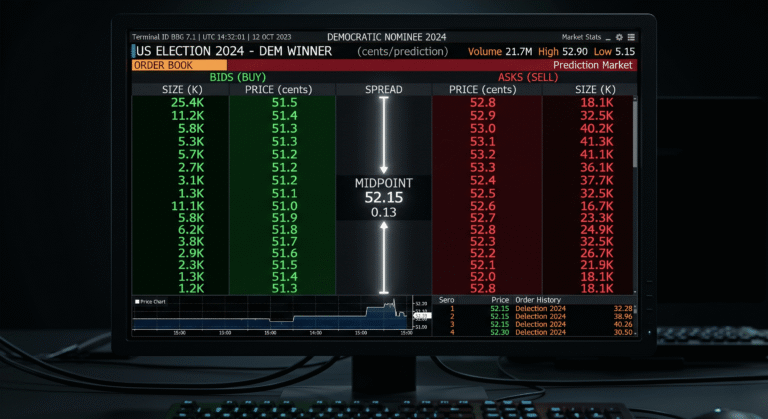

Polymarket calculates liquidity rewards using a Quadratic Spread Function that penalises orders placed far from the current market midpoint and rewards orders placed close to it. Understanding this formula directly determines how much capital to deploy and where to place orders to maximise returns.

The formula produces a reward score for each limit order based on three variables. The first variable is the distance from the midpoint. Specifically, an order placed at 49 cents when the midpoint is 50 cents receives a near-maximum score. An order placed at 47 cents when the midpoint is 50 cents receives a significantly reduced score. An order placed at 47 cents or further from the midpoint when the maximum spread is 3 cents falls outside the qualifying range entirely and earns zero rewards regardless of its size.

The second variable is the order size in USDC. Specifically, larger orders within the qualifying spread receive proportionally larger reward scores. A $10,000 limit order at 49 cents earns roughly 10 times the reward of a $1,000 limit order at the same price, all else equal. However, size only increases rewards when the order is within the maximum spread. A $100,000 order placed outside the qualifying range earns nothing.

The third variable is the double-sided bonus for tight quoting. Specifically, placing both a YES limit order and a NO limit order simultaneously in the same market earns a bonus multiplier on the total reward score. This bonus is the most important incentive structure in the entire program for experienced liquidity providers.

The Maximum Spread Boundary

The maximum spread for most Polymarket liquidity programs in 2026 is plus or minus 3 cents from the current midpoint. Specifically, if the midpoint is 50 cents, qualifying orders must be placed between 47 and 53 cents. Orders outside this range are completely excluded from reward calculations.

This boundary creates a practical operational requirement: your orders must move with the midpoint or they exit the reward zone. Specifically, if you place YES limit orders at 49 cents and the midpoint shifts to 54 cents after a news event, your 49-cent orders are now 5 cents from the new midpoint and outside the 3-cent qualifying boundary. At that point, rewards stop accruing until you cancel and replace the orders within the new qualifying range.

Daily Payout Structure

Rewards are calculated every minute and accumulated throughout the day. Payouts drop into your Polygon wallet address every 24 hours at midnight UTC. Specifically, you receive USDC directly to the wallet address connected to your Polymarket account. No claiming action is required on most market programs. Furthermore, the USDC is immediately accessible and usable for redeployment into new limit orders on the following day.

Step-by-Step: Setting Up Your First Liquidity Position

Step 1: Find Incentivised Markets Using the Blue Medal Icon

Not every Polymarket market offers liquidity rewards. Specifically, look for the blue medal icon on market cards when browsing the Polymarket interface. This icon indicates the market is part of an active liquidity incentive program. Click through to the market detail page to confirm the current APY and daily reward pool size before deploying any capital.

High-volume markets with confirmed reward programs in 2026 include US election-related markets, Federal Reserve rate decision markets, major cryptocurrency price markets, and high-profile sports championship outcomes. Additionally, newly launched markets occasionally offer elevated reward pools in the first days after launch to attract initial liquidity, which creates the highest yield-per-dollar opportunities covered in the pro tips section below.

Step 2: Check the APY and Daily Reward Pool

Each incentivised market displays a current APY figure and a total daily reward pool in USDC. Specifically, the APY is calculated based on the total rewards distributed daily divided by the total qualifying liquidity currently in the order book. As more liquidity providers enter the market, the APY decreases because the same reward pool is shared across a larger capital base.

High-volume markets like US Elections and Fed rate decisions typically show APY between 15% and 50% in 2026 when competition among liquidity providers is moderate. Newly launched markets with high reward pools and few competitors can show APY of 60% to 80% or higher in the initial days. Specifically, these newly launched markets represent the highest-priority opportunity for yield-maximising liquidity providers because the reward pool is fixed while the qualifying capital base is still small.

Before deploying capital, compare the APY against the qualifying spread boundary. Specifically, a market offering 60% APY with a 2-cent maximum spread requires more active order management than a market offering 20% APY with a 5-cent maximum spread. The higher APY is only realisable if you maintain orders within the tighter qualifying range, which requires either manual monitoring or automated management.

Step 3: Place Your Tight-Quote Position

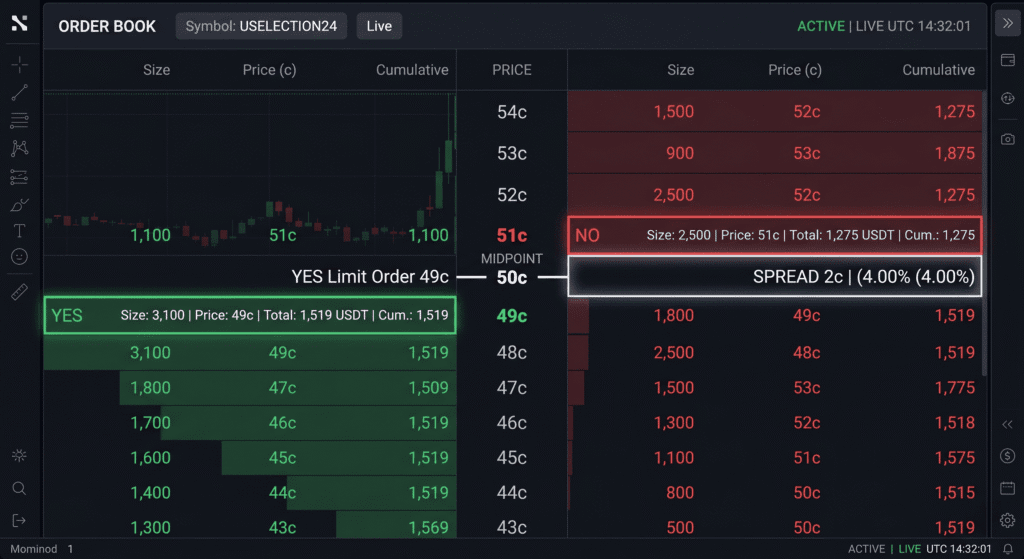

The standard tight-quote setup for a 50-cent midpoint market uses the following order structure. Place a YES limit buy order at 49 cents. Place a NO limit buy order at 49 cents (equivalently, a limit sell order on YES at 51 cents). This positions you with qualifying orders on both sides of the midpoint, capturing the double-sided bonus and the 1-cent spread from both directions.

Specifically, the 49 and 51 cent placement sits 1 cent from the midpoint on each side, well within the 3-cent maximum spread boundary, and earns near-maximum reward scores on the quadratic formula while also capturing 2 cents of spread income on any orders that fill.

For markets with higher volatility or wider natural spreads, adjust the placement to 48 and 52 cents rather than 49 and 51 cents. This slightly wider placement reduces reward score per order but provides more buffer against midpoint shifts before your orders exit the qualifying range.

Step 4: Monitor and Rebalance as the Midpoint Moves

Set a manual monitoring schedule or an automated alert for midpoint shifts above 2 cents from your current order placement. Specifically, a 2-cent midpoint shift against a 1-cent tight-quote placement puts your orders 3 cents from the new midpoint and at the edge of the qualifying boundary. A further 1-cent shift removes them entirely.

Cancel and replace orders whenever the midpoint shifts by 2 cents or more from your current placement. Specifically, always replace within the new 1-cent window around the updated midpoint to maintain near-maximum reward scores. The gas cost of cancelling and replacing orders on Polygon is negligible relative to the reward income lost from sitting outside the qualifying range.

The Three Genuine Risks of Polymarket Liquidity Mining

Toxic Flow: The Whale Sweep Problem

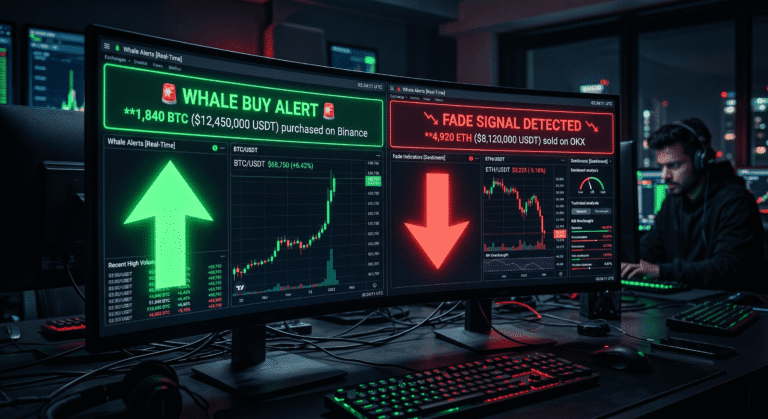

Toxic flow is the primary risk that separates profitable market makers from unprofitable ones. Specifically, toxic flow occurs when a directional trader with better information than you fills your limit orders before you can react to the information asymmetry.

The mechanics are as follows. You have placed a YES limit order at 49 cents on a geopolitical market. A wallet with insider knowledge of an imminent news event buys every available YES order in the book at 49 cents or lower before the news breaks publicly. Your 49-cent YES order fills immediately. The news breaks and the market midpoint jumps to 75 cents within minutes. You now hold YES shares that cost you 49 cents in a market you did not intend to hold as a directional position, and the informed buyer has captured the move from 49 to 75 cents at your expense.

This is precisely the dynamic described in the Iran ceasefire insider trade documentation. The four insider wallets who bought YES at 2.9 to 10.3 cents were filling the limit orders of existing liquidity providers who had no idea the ceasefire was imminent. The liquidity providers’ orders filled at the bottom of the range and they found themselves holding YES shares at a cost basis that was already below the post-announcement price.

Three practices reduce toxic flow risk specifically in Polymarket liquidity programs. First, avoid providing liquidity in geopolitics and political markets during periods of elevated news risk. Specifically, reduce or remove limit orders in election markets during debate periods, in conflict markets during active military operations, and in regulatory markets during scheduled policy announcements. Second, monitor the Polymarket whale alert system for unusual large directional buys that sweep through your side of the order book. A sweep rather than a gradual fill pattern signals informed capital rather than routine directional trading. Third, prioritise sports and crypto price markets over geopolitics markets for liquidity provision because the information asymmetry available to insiders is structurally lower in outcomes determined by athletic performance or algorithmic price feeds.

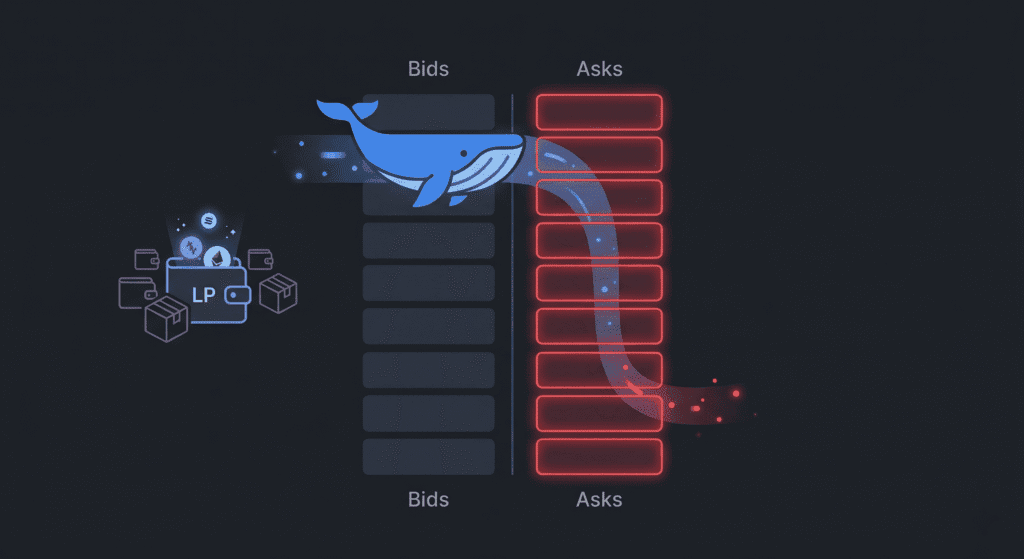

Inventory Risk: The One-Sided Fill Problem

Inventory risk arises when all your limit orders on one side fill while your other side remains unfilled, leaving you with 100% exposure to one outcome. Specifically, if every YES limit order at 49 cents fills because multiple traders simultaneously buy YES, you now hold a position that behaves identically to a directional YES bet without any NO offset.

The standard mitigation is position size limits per market. Specifically, never deploy more than 15 to 20% of your total liquidity capital in any single market. This cap ensures that even a complete one-sided fill in one market represents a manageable directional exposure rather than a portfolio-defining event. Furthermore, set a maximum total position size in each market category rather than just each individual market. A sports-category cap of 30% of total capital prevents correlated one-sided fills during high-activity sports periods from overwhelming your portfolio simultaneously.

Additionally, treat any one-sided fill that leaves you holding greater than 70% YES or 70% NO in a single market as an active position requiring management rather than a passive liquidity position. Specifically, either hedge the exposure (covered in the Hyperliquid section below) or set a stop-loss level at which you exit the position rather than holding to resolution.

The Midpoint Shift: Silent Reward Termination

The midpoint shift risk is the least dramatic but most consistently damaging risk for passive liquidity providers who do not monitor actively. Specifically, when the market midpoint moves outside your order placement range, your orders stop earning rewards silently without any notification unless you have a monitoring system in place. The orders remain in the book and may still fill, but they are no longer contributing to your reward score.

In a market paying 40% APY, a 24-hour period outside the qualifying range represents approximately 0.11% of capital lost in opportunity cost. Across a week of unmonitored midpoint drift, this produces 0.77% in missed rewards. At $50,000 deployed, this is $385 per week in foregone income from a problem that a 2-minute order replacement operation would have prevented.

Set automated alerts using the Cielo Finance wallet tracking system or a dedicated price alert tool to notify you whenever a tracked market’s midpoint moves 2 cents or more from your current order placement. This alert threshold gives you time to reposition before your orders exit the qualifying boundary rather than after.

Pro Tips for Advanced Liquidity Providers in 2026

Jito-Style Automated Order Management

Professional liquidity providers in 2026 do not manually reposition orders when the midpoint shifts. Instead, they run automated scripts that monitor the Polymarket CLOB API in real time and cancel and replace limit orders within milliseconds of a qualifying midpoint shift. This approach, described in the Polymarket community as Jito-style monitoring after the Solana MEV infrastructure it resembles, ensures that orders never exit the qualifying reward range regardless of how fast the midpoint moves.

The technical implementation uses Polymarket’s public CLOB API endpoint at https://clob.polymarket.com combined with a Python script using the py_clob_client library. Specifically, the script subscribes to price updates for tracked markets, calculates whether current orders remain within the qualifying spread on each update, and replaces orders automatically when the qualifying boundary is breached. The Polygon gas cost of each cancel-and-replace operation is approximately $0.001 to $0.005, which is negligible against the reward income preserved by maintaining continuous qualification.

For traders without Python experience, a simpler version of this workflow uses the DropsBot price threshold alert system to trigger a manual notification at 2-cent midpoint movements, as described in the whale alerts setup guide. This semi-automated approach adds 5 to 15 minutes of lag versus the fully automated script but eliminates the technical barrier for non-developers.

The Low-Competition Newly Launched Market Strategy

The highest yield-per-dollar opportunity in Polymarket liquidity mining consistently appears in newly launched markets during their first 48 to 72 hours of existence. Specifically, when Polymarket launches a new incentivised market with a fixed daily reward pool and few liquidity providers have discovered it yet, the APY can reach 60% to 120% because the same reward pool is distributed across a very small capital base.

The identification method is straightforward. Check the Polymarket market discovery feed sorted by newest first each morning. Specifically, look for newly listed markets with the blue medal reward icon that show a daily reward pool above $500 USDC and total qualifying liquidity below $50,000. At these parameters, a $5,000 deployment captures 10% of the qualifying liquidity and receives 10% of the daily reward pool, which at $500 daily translates to $50 per day on $5,000 deployed, or 365% APY before any spread income.

This opportunity degrades rapidly as more liquidity providers discover the market and increase the qualifying capital base, which dilutes each provider’s share of the fixed reward pool. Specifically, the window of maximum opportunity is typically 24 to 72 hours after launch before APY normalises toward the 15% to 50% range seen in established markets. Daily monitoring of new market launches is the only reliable method for capturing this alpha consistently.

The Hyperliquid Hedge: Removing Outcome Risk Entirely

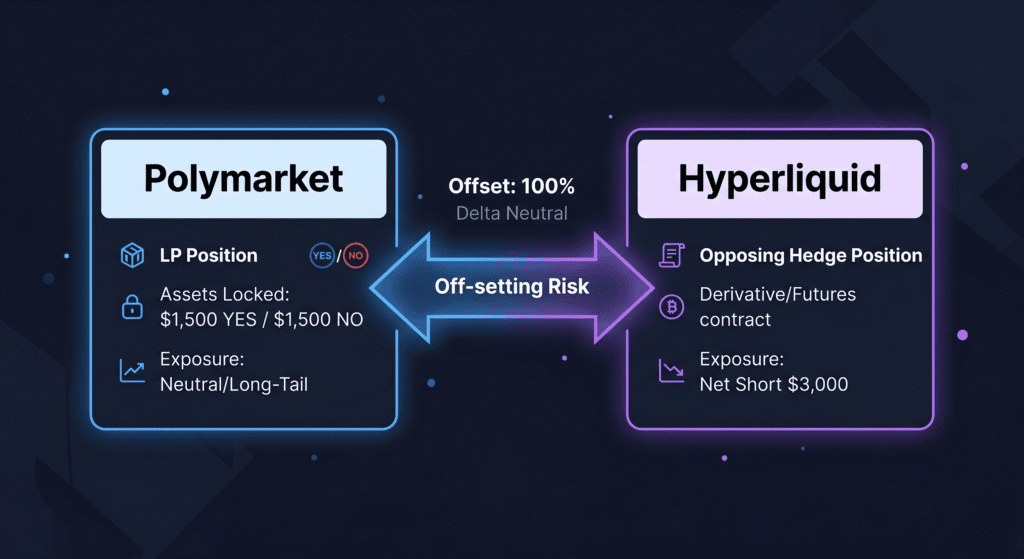

The most sophisticated liquidity provision strategy in 2026 combines a Polymarket liquidity position with an offsetting position on Hyperliquid to neutralise inventory risk and directional exposure entirely, leaving only the reward income as net return.

The mechanics work as follows. You deploy $10,000 in tight-quote liquidity on a political market with a 50-cent midpoint. If all your YES orders fill and you find yourself holding $10,000 in YES shares with directional exposure, you simultaneously open a short position on the underlying outcome or a correlated asset on Hyperliquid. Specifically, for a political market correlated with cryptocurrency price movements (such as a Federal Reserve rate decision), a short on BTC or ETH via Hyperliquid perpetuals hedges the inventory risk created by your one-sided YES fill.

The hedge is not perfect because Polymarket outcomes and Hyperliquid perpetual prices have imperfect correlation. However, for high-correlation markets, the hedge removes 60 to 80% of the inventory risk while preserving the full USDC reward income stream. Furthermore, if the political market outcome is itself directly hedgeable on Hyperliquid through prediction market-adjacent perpetuals, the hedge can approach 90% correlation and nearly full inventory risk elimination.

The net return profile of the hedged strategy is USDC reward income at 15% to 80% APY minus the cost of the Hyperliquid hedge position (funding rate plus spread costs, typically 5% to 15% annualised). The net after hedging costs is 10% to 65% APY on deployed capital with dramatically reduced directional outcome risk. For capital-efficient traders who want yield without binary outcome exposure, this hedged structure is the closest available approximation to pure market-making returns on Polymarket.

Choosing the Right Markets for Liquidity Mining

The correct market selection framework for Polymarket liquidity mining balances four variables: reward APY, toxic flow risk, midpoint volatility, and competition density.

Sports markets and cryptocurrency price markets score highest on the toxic flow risk dimension because the information asymmetry available to insiders is structurally lower than in geopolitics or political markets. Additionally, these markets typically resolve on predictable schedules (game end times, daily price snapshots), which allows precise order management around resolution periods. Specifically, remove liquidity positions 30 to 60 minutes before resolution in any market to avoid holding inventory through the final binary outcome.

Geopolitics and political markets offer the highest reward APY but carry the highest toxic flow risk. These markets are appropriate for experienced liquidity providers who have an active monitoring system and can respond to order sweeps within minutes. They are not appropriate for passive set-and-forget strategies without automated rebalancing.

Newly launched markets in any category offer the highest temporary APY for the 24 to 72 hour window described above. These are appropriate for all experience levels because the short deployment window limits the accumulated directional risk from inventory imbalance.

High-liquidity established markets like Fed rate decisions and US elections offer the lowest APY but the most predictable reward income because the large existing order book smooths out midpoint volatility and reduces toxic flow impact per individual provider’s position. These markets are appropriate for large capital deployments where absolute USDC return matters more than percentage yield.

Key Takeaways for CoinTrenches Readers

Polymarket liquidity mining in 2026 is a genuinely distinct income strategy from directional prediction market betting. Specifically, the reward formula, the double-sided tight-quoting bonus, and the daily USDC payout structure create a compounding yield opportunity that requires no ability to predict outcomes and no willingness to take binary directional risk as long as inventory risk is actively managed.

The quadratic spread formula makes placement precision more important than raw capital size. Specifically, $5,000 deployed at 1 cent from the midpoint earns more than $5,000 deployed at 3 cents from the midpoint. Understanding the qualifying boundary and staying within it consistently produces more reward income than simply deploying more capital carelessly.

Toxic flow is the non-negotiable risk that every Polymarket liquidity provider must manage. Specifically, geopolitics markets during active news periods are the highest-risk environments for uninformed market makers. The Iran ceasefire insider pattern is the documented case study. Running an active whale alert system alongside your liquidity positions is not optional for anyone providing liquidity in political or geopolitical markets.

The newly launched market strategy is the highest-yield opportunity available without sophisticated hedging infrastructure. Check new market listings every morning, identify incentivised markets with large reward pools and small existing liquidity bases, deploy for 24 to 72 hours, and redeploy when APY normalises. This routine produces consistently above-market yield without requiring any of the advanced automation or hedging infrastructure described in the pro tips section.

Frequently Asked Questions

What is Polymarket liquidity mining?

Polymarket liquidity mining is the practice of earning daily USDC rewards by placing limit orders in Polymarket prediction markets that have active liquidity incentive programs. Specifically, Polymarket pays liquidity providers based on how close their orders are to the current market midpoint and how large those orders are, using a Quadratic Spread Function that calculates a reward score every minute. Rewards accrue continuously and are paid out daily at midnight UTC into the provider’s Polygon wallet, regardless of whether the underlying market outcome resolves in the provider’s favor.

How much can I earn from Polymarket liquidity mining in 2026?

APY varies significantly by market and competition level. High-volume established markets like US Elections and Fed rate decisions typically offer between 15% and 50% APY when competition among liquidity providers is moderate. Newly launched markets with large reward pools and few providers can offer 60% to 120% APY for the first 24 to 72 hours. Specifically, the APY decreases as more capital enters the qualifying order book because the same daily reward pool is shared across a larger base. Active monitoring of new market launches is the most reliable method for capturing the highest yield opportunities.

What is tight quoting on Polymarket?

Tight quoting refers to placing both a YES limit order and a NO limit order simultaneously in the same market, positioned symmetrically close to the current midpoint. Specifically, the standard tight-quote setup places YES at 49 cents and NO at 51 cents when the midpoint is 50 cents. This double-sided positioning earns a bonus multiplier on the Quadratic Spread Function reward score compared to one-sided limit order placement, and it also captures 2 cents of spread income on any orders that fill. Tight quoting is the highest-reward configuration available in Polymarket’s liquidity incentive program.

What is toxic flow risk in Polymarket liquidity mining?

Toxic flow risk is the danger that an informed directional trader fills your limit orders using information you do not have access to. Specifically, if a whale with insider knowledge of an imminent news event buys all available YES shares at your limit price before the news becomes public, your order fills at a disadvantageous price and you are left holding YES inventory in a market that resolves against you. The Iran ceasefire insider trade documented in April 2026 is the clearest case study: insider wallets swept through limit orders at 2.9 to 10.3 cents before the announcement, filling the positions of uninformed liquidity providers at prices far below the post-announcement resolution value.

How do I hedge my Polymarket liquidity position on Hyperliquid?

When a one-sided fill leaves you holding directional inventory from a Polymarket liquidity position, open an offsetting position on Hyperliquid to neutralise the outcome exposure. Specifically, for markets correlated with cryptocurrency price movements such as Federal Reserve rate decisions, a short perpetual position on BTC or ETH via Hyperliquid hedges the inventory risk from a one-sided YES fill. The hedge removes approximately 60% to 80% of directional risk for high-correlation markets. Net returns after hedge costs (funding rate plus spread, typically 5% to 15% annualised) remain 10% to 65% APY on deployed capital, depending on the original market’s reward rate.

What is the maximum spread for Polymarket liquidity rewards?

The maximum qualifying spread for most Polymarket liquidity reward programs in 2026 is plus or minus 3 cents from the current market midpoint. Specifically, if the midpoint is 50 cents, only limit orders placed between 47 and 53 cents receive any reward score from the Quadratic Spread Function. Orders placed outside this range earn zero rewards regardless of their size. Within the qualifying range, orders placed closer to the midpoint earn progressively higher reward scores, with orders at the midpoint itself earning the maximum possible score. This boundary requires active order management because the midpoint shifts continuously as trades execute.

Keep Reading on CoinTrenches

Real-Time Polymarket Whale Alerts: Full Setup Guide 2026 — the essential companion system for detecting toxic flow before it sweeps through your liquidity positions

How to Find Polymarket Whales on Polygonscan: Full Guide 2026 — the on-chain research method for identifying the wallets most likely to generate toxic flow in your active markets

Copy-Trading Polymarket Whales: When to Follow and When to Fade — the directional trading companion to this guide, covering how to profit from the same whale movements that threaten your liquidity positions

Polymarket Insider Traders: $663K on Iran Ceasefire in One Bet — the documented toxic flow case study that every Polymarket liquidity provider should study before deploying capital in geopolitics markets

Theo4 Polymarket: $22M Profit, 14 Bets, $19 in Losses — the highest all-time profit wallet on the platform and the most important address to monitor for toxic flow risk when providing liquidity in political markets

sovereign2013 Polymarket: $3.4M All-Time, Sports Bot Full Profile — the confirmed high-frequency sports bot whose order flow in NBA and NCAA markets represents the dominant directional activity that liquidity providers in sports categories must account for